Kyle Ryan, CFP®, ChFC®, is a co-owner and financial planner at Menninger & Associates Financial Planning. He provides his clients with financial products and services, always with his client's individual needs foremost in his mind.

Continuing education courses can help you change careers, increase income, or reenter the workforce. These courses are often a cost-effective way to enhance your career, but unless you can pay in cash, you must find a way to fund them.

Student loans can help. You might be eligible for federal, private, or both loans depending on your program and where you attend.

| Lender | Best for | Enrollment req. |

| Dept. of Education | Federal student loans | Half-time |

| College Ave | Private student loans | Part-time |

| Sallie Mae | Cosigners | Part-time |

| Ascent | No cosigners | Half-time |

As a continuing education student, you may be eligible for various federal loans but must meet the following eligibility requirements.

You must complete the Free Application for Federal Student Aid (FAFSA) to check your eligibility for federal loans. Completing the application means you might be eligible for a federal loan, including Direct Subsidized Loans, Direct Unsubsidized Loans, and PLUS Loans.

| Loan | Interest rate | Annual limit |

| Subsidized Loan | 6.53% | Undergrad: $3,500–$5,500 (varies by academic year) |

| Unsubsidized Loan | 6.53% (undergrads), 8.08% (grads & professionals) | Undergrad: $5,500–$12,500; Grad: $20,500 |

| Direct PLUS Loan | 9.08% | Cost of attendance minus any financial aid |

First-year students may be eligible to borrow up to $3,500 and $5,500 for Subsidized and Unsubsidized Loans, respectively; the limit increases up to your third academic year.

Unsubsidized Loans have an exception for independent students and dependent undergrads whose parents don’t qualify for the Parent PLUS Loan: Their limits start at $9,500 versus $5,500 for dependents.

The aggregate, or combined total, limit for undergrads, graduates, and professionals are:

As you search for federal student loans, ask your institution for advice. Most continuing education programs have a financial aid office or counselor who can provide guidance.

Private student loans can also help with the costs of your education. Unlike federal loans, some private lenders don’t require half-time enrollment.

You usually need a good credit score to qualify for a private student loan. If you don’t have a solid credit score, you may need a cosigner to help you qualify.

Although the top private student loan lenders offer low starting rates, borrowers with poor-to-average credit scores often get approved at much higher rates than federal loans. With excellent credit, you or a cosigner may be able to take advantage of these starting rates.

Here are the top private student loan lenders for continuing education costs.

College Ave offers a Career Loan for students pursuing associate’s, bachelor’s, graduate, and graduate health degree programs. The application process is simple, and you can apply with or without a cosigner. You can also score periodic cash-back bonuses applied to your loan balance.

You can borrow enough to cover the school’s attendance cost, including funds for living expenses and school bills. You must attend at least half-time to take advantage of College Ave’s six-month grace period. This period starts when you leave school and ends when your first full payment is due.

| Rates (APR) | 4.17 % – 17.99 % |

| Loan amounts | $1,000 – 100% of attendance costs |

Best for cosigners

LendEDU RatingWith undergraduate loans, certificate loans, and specialized graduate student loans for various professions, Sallie Mae offers the most options for continuing education. Students can attend less than half-time, which provides additional flexibility. But you or your cosigner must meet the lending requirements, including a solid credit score.

The Smart Option Student Loan feature for Career Training means you’ll apply once for a year of trade school or professional training costs. Plus, you can release a cosigner after 12 months of on-time payments—faster than most lenders.

| Rates (APR) | 4.17 % – 17.99 % |

| Loan amounts | $1,000 – 100% of attendance costs |

Best for no cosigners

LendEDU RatingIf you’re looking for student loans for continuing education, Ascent has two options: boot camp and career loans. These loan options are for students attending professional training and certification programs at select schools. Students can also earn 1% cash back after graduating, which reduces their loan balance.

Ascent doesn’t disclose a minimum credit score, but the company states that student borrowers without cosigners must have at least two years of credit history. The minimum loan amount is $2,001; the maximum is $200,000 for undergrads and $400,000 for graduates.

| Rates (APR) | 3.79% – 15.85% |

| Loan amounts | $2,001 ($6,001 for MA) – $400,000 for graduates for credit-based loans |

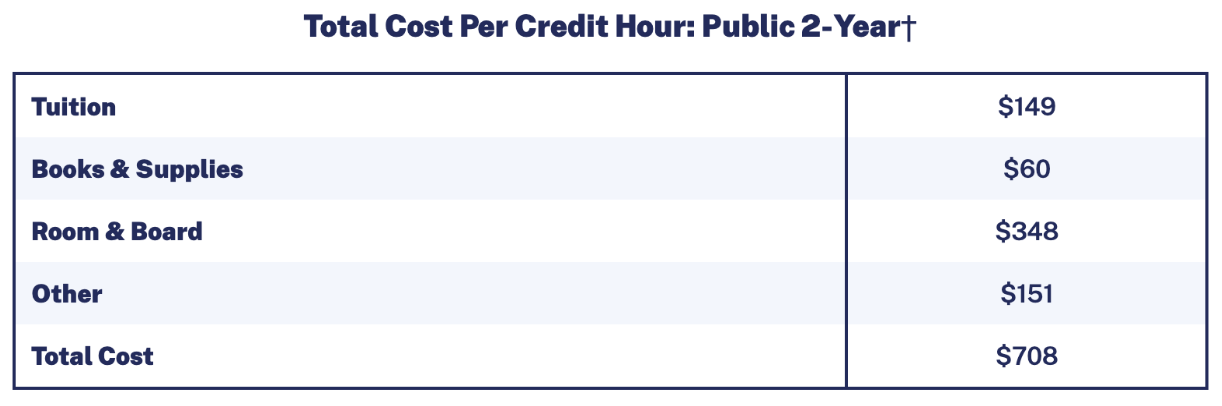

On average, your total cost to go to a two-year postsecondary institution in state would cost you $708 for each credit, according to the Education Data Initiative. That’s almost $4,300 per semester for a part-time student and $8,500 for full-timers.

When you take out student loans for continuing education, you invest in your future. Be sure you understand the long-term effects of this commitment.

The total cost of your loan goes far beyond the amount you borrowed and includes interest and fees. If we just focus on interest, we can see the implications. Interest can increase how much you pay over the life of your loan.

The two main types of interest rates are:

If a $10,000 loan with a fixed interest rate of 5% has a standard 10-year repayment term, the total amount you repay by the end of the term includes your principal amount plus the interest accrued over the 10 years—according to our student loan calculator, it could cost an additional $2,728.

Don’t be hasty if you’re considering taking out additional student loans. The more you borrow, the more your overall debt will be, which could make paying it back more difficult.

For example, if you have a federal loan with a $15,000 balance at a 6.00% interest rate, you’re looking at a $167 monthly payment. Add another $10,000 loan at a 5.00% interest rate, and you assume another $106 monthly payment––$273 in combined monthly payments.

The average student loan borrower owes more than $40,000 in federal and private debt. So before you take on more debt:

Expert advice on managing current student loan debt while considering additional loans

This all comes down to cash flow and opportunity cost. The first thing to ask oneself is, “Why am I seeking continuing education?” If the answer is a higher income, look at your cash flow and continuing education costs to see whether you can afford it. If you need loans, it requires balancing out what that increased income may be versus the additional cost of the education. Not all fields have a positive return on the cost of education. Deferment of loans is another important consideration. If going to school allows you to defer your loans, will you be able to get a higher-paying job once payments resume that can help you afford the cost of the additional loans?

Whether you should take out student loans for continuing education depends on your situation.

Whichever decision you make, ensure that you can pay off your loans without unnecessary stress and continue to make progress in other areas of your life

| Consider continuing education loans if… | Consider an alternative if… |

| Your program shows a high earning potential. | The financial strain overshadows the benefits. |

| You’ve mapped out a repayment plan that won’t stretch you too thin. | You have cheaper options, such as online courses, scholarships, or employer-sponsored programs. |

| You qualify for favorable loan terms, such as low interest rates and practical terms you can take advantage of to pay the loan off quickly | You’re unsure about your career path, or you’re better off saving up for a few years and starting later |

Follow these steps to apply for a federal student loan.

To set up an online account, enter your personal information.

Fill out and submit the FAFSA by June 30 for the current school year. Your school and state deadlines vary, so check those too.

Select as many as 20 schools to find out what student aid each may offer. (You can confirm whether the U.S. Department of Education considers your school an eligible institution using the Database of Accredited Postsecondary Institutions and Programs or the Federal School Code Search.)

It may take up to a week to process your application. Afterward, you’ll receive the FAFSA Submission Summary of financial aid you may be eligible for. Review the summary and make sure there are no mistakes.

The schools you chose will send you financial aid offers detailing the cost of attendance and your deadline to accept.

Once you know where you’d like to attend, notify the school by following its instructions and accept the financial aid offers you’d need. Accept your financial aid in this order:

Once you’ve exhausted funding through federal student loans, grants, and scholarships, if you need more funding for your continued education, you can take the following steps to apply for private student loans:

The lender will attempt to verify your identity once you enter your personal information and details about your school or program, including when you’ll attend, attendance costs, and the loan amount you need.

Many borrowers are more likely to get approved with a cosigner. The lender will allow you to apply with or without one. If you apply with a cosigner, they must fill out a separate part of the application.

Be sure your cosigner understands they’re committing to paying for your loan if you don’t.

Enter your employment status and annual income.

You can view the interest rates you prequalify for after submitting your application.

If you’re approved, the lender will let you know when to expect funding.

Your school should get the funds on your behalf within the first few weeks of the start of the semester.

We have more resources to assist you if you’re looking for additional help financing your continuing education.

See below for a variety of program-specific loans and financing products:

You have options if you’re not sold on student loans or need additional funds. But before considering loans or alternatives, research scholarships and grants that offer free money. You might be able to find a scholarship or grant specific to your chosen career path.

Once you’ve exhausted your free options, consider the following alternatives to student loans for continuing education.

Your employer is the best place to start! If the continuing education is for your current job, your workplace may be incentivized to help support your career growth.

Yes, you can use the FAFSA to pay for a certificate program from an accredited institution participating in federal student aid programs. Eligible students can get federal grants, loans, and work-study funds to help cover the cost of their certificate programs. It’s important to verify the institution and program’s accreditation and federal aid eligibility before applying.

Yes, you can get a student loan for more than your tuition. Federal and many private student loans can cover tuition and other education-related expenses, such as room and board, books, supplies, transportation, and personal expenses. The total amount you can borrow is typically capped by the cost of attendance determined by your school minus any other financial aid you receive.

The number of years you’re eligible for federal student loans depends on the type of loan and your academic program. Federal Direct Subsidized and Unsubsidized Loans have annual and aggregate limits for undergraduate students. You may be able to take out up to 150% of the published length of your program (e.g., six years for a four-year degree). Graduate and professional student loans have annual and aggregate loan limits but no fixed number of years. Eligibility continues if you meet the requirements and haven’t exceeded the aggregate loan limits.

Financial aid can cover a second bachelor’s degree, but eligibility for certain types of aid may be limited. Federal Pell Grants, for example, are available only for the first bachelor’s degree. However, you may still be eligible for Direct Loans, federal work-study, and other federal, state, or institutional aid for a second bachelor’s degree. Check with your school’s financial aid office to understand your options and limitations.

LendEDU evaluates student loan lenders to help readers find the best student loans. Our latest analysis reviewed 725 data points from 25 lenders and financial institutions, with 29 data points collected. This information is gathered from company websites, online applications, public disclosures, customer reviews, and direct communication with company representatives.

These star ratings help us determine which companies are best for different situations. We don’t believe two companies can be the best for the same purpose, so we only show each best-for designation once.

| Lender | Best for |

| Dept. of Education | Federal student loans |

| College Ave | Private student loans |

| Sallie Mae | Cosigners |

| Ascent | No cosigners |